The page you are looking for cannot be found.

View All Properties

2019 N 20th Street, Omaha, NE, 68110

6711 Wren Circle, Papillion, NE, 68133

13121 W Rokeby Road, Denton, NE, 68339

208 Lincoln Avenue, MALVERN, IA, 51551

7401 W Olive Creek Road, Hallam, NE, 68368

308 N 9th Steet , Norfolk, NE, 68701

1203 E Airport Rd , Grand Island, NE, 68801

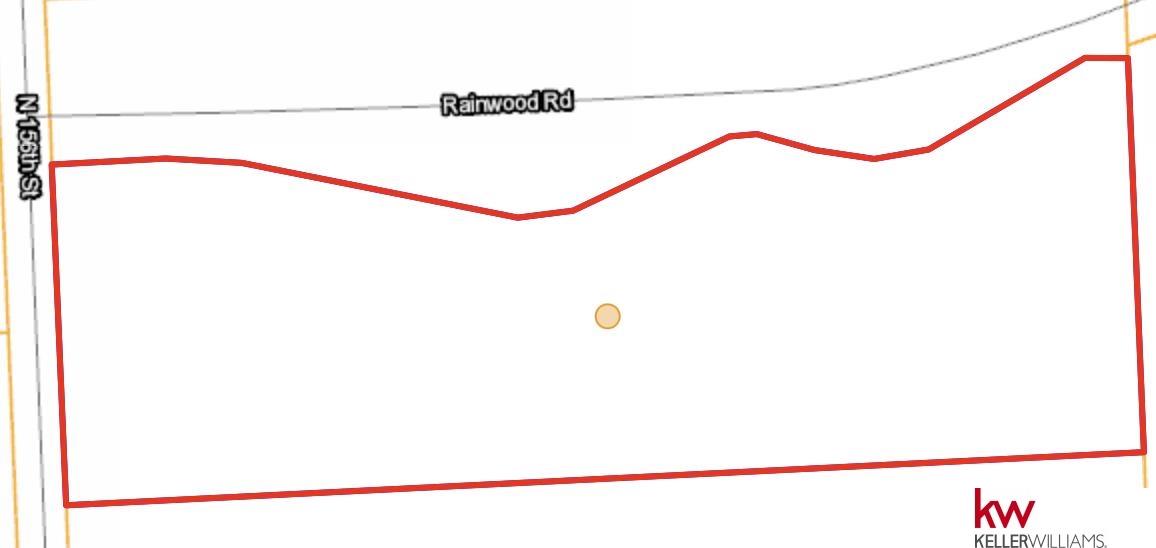

TBD N 156th Land, Bennington, NE, 68007